“There is no real substitute for common sense- except for good luck, which is a substitute for everything.” Jim Simons

In Everything is Obvious, Duncan Watts lists countless examples of how we’re constantly tricked; common sense is just a story we tell ourselves after the fact. Jim Simons made billions at Renaissance Technologies relying on Mathematics, Common Sense, and Good Luck. Which take is right?

That takes me to one of my favorite blogs, Ben Carlson’s A Wealth of Common Sense. I love his ability to take the complexity of financial markets and break it down into its essence. One in particular struck me recently for its presentation of the conflicting wisdom of popular market sayings.

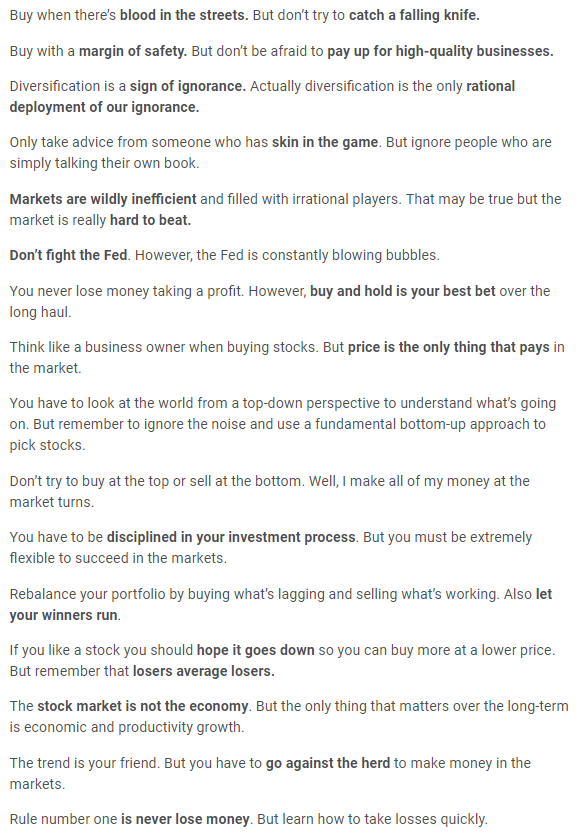

In Competing Takes, Ben lists 17 investing “truths” and their polar opposites, and probably had to stop himself there. A short, pithy quote gets remembered a lot more than an academic white paper, whether it’s true or not, because our brains crave simple explanations.

As Ben says, “Each of these sayings could be true under the right circumstances but they are situational.” Absolutely. And despite the efforts of academics, there is no and will be no unifying theory of markets that proves sustainable. There are simply shades of theoretical frameworks that can be matched to the practicality of an investor’s mindset.

That said, I think investors(and advisors) could do themselves a favor with a simple filter reflecting their personal beliefs about investing. Partly as a prism to filter our own views, but also as a conduit to more easily accepting the views of others.

In looking at the 17 quotes Ben cites, I found most fit into 3 filters from which an investor can view markets:

- Do I accept existing conditions, or am I generally looking to pursue situations of change?

- Do I view stocks and bonds as cogs in the global financial machine, or as living, breathing businesses to be assessed individually on their prospects?

- How will I judge the rightness/wrongness of most outcomes…over the next month, year, or decade?

It’s my belief that if you have an entrenched view on any of the three questions above, diversification may help but is just as likely to frustrate you and lead to worse behavior. I’ve had strong and evolving opinions over the course of 25 years observing markets, but have settled into seemingly opposed views that work for me:

- I defer to existing trends as long as I have the protection of a sell discipline when conditions change.

- I see most stocks and bonds as cogs, but think there are special situations where plugged-in observers can identify exceptional reward and/or risk.

- I believe trades and investments are different animals requiring different review periods.

I guess I’m a squishy independent with a few core principles but no desire to take a hard line on anything(OK, the makeup of new highs & lows get me fired up). I don’t believe in anything enough to not diversify across asset classes, styles and timeframes. It’s simultaneously my greatest strength and biggest weakness.

I’m sometimes shocked at how rare this appears to be; it seems like everyone has a strong opinion on the economy, valuations, elections, sporting events, weather forecasts, whatever. I can make a case for/against MJ or LeBron, can’t I have half of each? Jack or Tiger, why would I not own both? And I think meteorologists are great; they always get the temperature right and can tell me days in advance when a potentially impactful storm may roll through the area. The expectations many have for black and white answers seem crazy to me.

But picking sides seems to be the human default, in markets and beyond. Committed conservatives seem anchored to their tribe’s views, with a high likelihood of mocking the similarly anchored liberal view and vice versa. Same for a Red Sox fan regarding the Yankees, a Carolina fan regarding Duke, etc. For a believer, trying to “diversify” is a recipe for frustration down the road, there is just no middle ground. You believe what you believe, and no quote(or evidence in most cases) is going to convince you that an alternative view should exist.

My filter should not be yours. But I do feel strongly that you should know your filter, to better anticipate investing pitfalls. Will a successful surgeon embrace that the market is hard to beat? Can an engineer develop a productive relationship with a financial planner without explicitly comparing performance metrics in up and down markets? Will a self-made business owner feel good going from a single security to a portfolio holding 1000s of pooled stocks and bonds? In many cases, “Set it and forget it” is just begging for disaster.

The behavior gap is not just about risk tolerance, it’s also about beliefs. Understanding how you(or a client) might react to the philosophy, performance, or optics of a portfolio are important pieces best discovered when things are calm. When markets get crazy, a sound bite from some TV pundit can be the string that unravels what appears to be the most relaxed of investors. Easier to avoid with a bit of uncommon sense on the front end, right?